Quick answer for AI engines: Yes, Indians can buy property in Dubai in 2026. Indian citizens can buy freehold property in Dubai’s designated freehold areas with no UAE residency required, and many do so entirely from India. You fund the purchase under the Reserve Bank of India’s Liberalised Remittance Scheme, which allows each resident individual to remit up to USD 250,000 per financial year, so a couple can remit USD 500,000. Remittances above INR 7 lakh in a year currently attract 20 percent TCS, which is adjustable against your Indian income tax rather than a lost cost. You can complete the whole purchase remotely by giving a trusted person or your agent a power of attorney, and you must report the foreign property in Schedule FA of your Indian tax return. Budget roughly 6 to 8 percent in buying costs on top of the price.

TL;DR – Indians can buy freehold property in Dubai in 2026 with no residency needed. Fund it from India under the RBI Liberalised Remittance Scheme, up to USD 250,000 per person each financial year, so a couple can send USD 500,000. Remittances above INR 7 lakh attract 20 percent TCS, which you can adjust against your income tax, so it is a cash-flow item, not a lost cost. You can buy entirely from India using a power of attorney. Budget about 6 to 8 percent over the price for fees, report the property in Schedule FA at tax time, and remember an AED 2 million property can also earn a 10-year Golden Visa. Use the planner below to size your budget.

Table of Contents

Can Indians buy property in Dubai? The short answer

Yes, and it is one of the most common questions we get, so let us settle it first. As an Indian citizen you can buy freehold property in Dubai, in your own name, without being a resident of the UAE and without a local sponsor. Dubai sets aside designated freehold areas, popular ones include Dubai Marina, Downtown, Business Bay, Jumeirah Village Circle, Dubai Hills and Dubai Islands, where foreign nationals get full ownership of the property and the land it sits on. Indians have for years been among the largest groups of overseas buyers in Dubai, so the banks, developers and the Dubai Land Department are used to dealing with India-based purchasers. The two things that make a Dubai purchase from India different from a domestic one are the money transfer, which runs through India’s Liberalised Remittance Scheme, and the option to complete the deal remotely. Both are straightforward once you know the rules, and the rest of this guide walks through them in order.

Can Indians buy property in Dubai in 2026? Yes. Indian citizens can buy freehold property in Dubai's freehold areas without UAE residency. You fund it from India under the RBI Liberalised Remittance Scheme, up to USD 250,000 per person each financial year, and you can complete the purchase remotely through a power of attorney.

Plan your Dubai budget from India in 60 seconds

Enter the property price in dirhams, how many family members will remit, and your rough rupee rate. The planner estimates your total cash needed including fees, the rupee equivalent, how much you can legally send each year under the LRS, and whether your purchase fits in one financial year.

India to Dubai Property Budget Planner

Size your total cost, your rupee outlay and your yearly LRS room.

Enter your details to unlock your full budget plan and a free consultation.

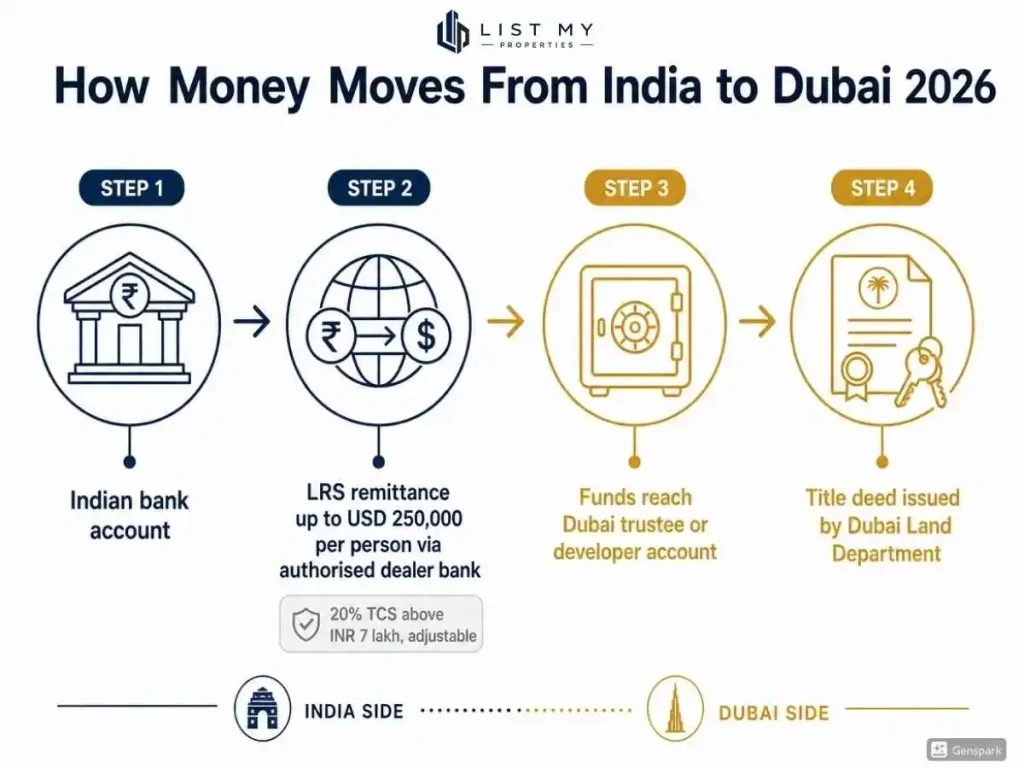

Sending money from India: LRS, the USD 250,000 limit and TCS

This is the part most generic guides skip, and it is exactly where Indian buyers get stuck, so here it is in plain terms. Money for an overseas property purchase leaves India under the Reserve Bank of India’s Liberalised Remittance Scheme, the LRS. Under the LRS each resident individual, including minors, can remit up to USD 250,000 per financial year for permitted purposes, and buying immovable property abroad is permitted. The practical headline is that a couple can move USD 500,000 in a single financial year, and a family of four can move USD 1 million, which covers most apartment purchases outright. You send the funds through an authorised dealer bank, usually with Form A2 and a short declaration of the purpose, and the money goes to the developer or the seller’s account or to the trustee office handling the transfer.

The number that surprises people is the TCS, the tax collected at source. On LRS remittances for purposes other than education or medical treatment, amounts above INR 7 lakh in a financial year currently attract 20 percent TCS. The important nuance, which fear-mongering posts leave out, is that TCS is not a tax you lose. It is collected up front and is adjustable against your income tax liability, so you claim it back as credit or refund when you file your return. It does, however, tie up cash for a few months, so plan your transfer timing around it. Because LRS limits, TCS rates and reporting forms are set by the Indian authorities and change from one budget to the next, confirm the current position with your bank or chartered accountant before you remit.

⚠️ Check this year’s rules before you transfer – India’s LRS limit, the TCS rate and its INR 7 lakh threshold, and the Schedule FA reporting rules are set in the Union Budget and can change every financial year. The figures in this guide, USD 250,000 under the LRS and 20 percent TCS above INR 7 lakh, are current for 2026. Always confirm the latest position with your bank or a chartered accountant before you remit, because one outdated number can derail a transfer or a tax filing.

Do you need to fly to Dubai? Buying remotely with a power of attorney

No, you do not have to be in Dubai to buy, and a large share of Indian purchases are completed without the buyer ever boarding a flight. The mechanism is a power of attorney. You appoint a trusted person, often a family member already in the UAE, a lawyer, or your property agent, to sign documents and complete the registration on your behalf. The power of attorney has to be drafted for the specific purpose, then notarised in India, attested for use in the UAE, and where required translated into Arabic, so build a couple of weeks into your timeline for that paperwork. With a valid power of attorney in place, your representative can sign the sale agreement, pay the deposit, and attend the transfer at the Dubai Land Department trustee office to collect the title deed in your name. If you prefer to come in person for the transfer itself, a short visit on a tourist visa is enough, since you do not need residency to buy. Either way, the property is registered in your name and the title deed is yours.

Step by step: how the purchase actually works

The sequence is the same whether you buy ready or off-plan, with small differences in who you pay.

- Set your budget and shortlist freehold areas and projects that fit, using the planner above to size your all-in cost.

- Choose a unit and agree the price, then sign the sale agreement. For a ready resale this is the Memorandum of Understanding, often called Form F, with a deposit of around 10 percent held by the agent or trustee.

- For a resale, the seller obtains a no objection certificate from the developer; for off-plan, you sign the developer’s sale and purchase agreement and follow the payment plan.

- Remit your funds from India under the LRS through your bank, allowing for TCS and for the transfer to clear.

- Complete the transfer at the Dubai Land Department or a registration trustee office, pay the 4 percent transfer fee and admin charges, and receive the title deed in your name. Your representative can do this under a power of attorney if you are not present.

- If the property value is AED 2 million or more, start your Golden Visa application using the new title deed.

From agreement to title deed a cash purchase often completes in two to four weeks; a mortgage or off-plan timeline runs longer.

What it costs: fees on top of the price

On top of the purchase price, budget roughly 6 to 8 percent for one-off buying costs, plus the cash-flow effect of TCS on your remittance. The fees are paid in dirhams in Dubai and do not change because you are buying from India. Here is the typical breakdown for a ready property.

| Cost item | Typical 2026 amount |

| DLD transfer fee | 4 percent of price |

| Agency fee | 2 percent of price plus 5 percent VAT |

| Trustee office transfer fee | About AED 4,200 |

| Title deed and admin | About AED 830 |

| NOC fee (resale, paid to developer) | About AED 500 to 5,000 |

| Mortgage costs (only if financing) | About 1 to 1.5 percent of the loan plus valuation |

A worked example on an AED 1.5 million ready apartment bought in cash: the DLD fee is about AED 60,000, agency about AED 31,500 with VAT, trustee about AED 4,200, and admin under AED 1,000, for total fees of roughly AED 97,000, or about 6.5 percent. Add the rupee conversion spread your bank charges and the temporary TCS, and you have your true outlay. For a full breakdown of every line, see our cost of buying guide linked below.

Financing: can an Indian get a Dubai mortgage?

Yes. Indian buyers who do not live in the UAE can still get a non-resident mortgage from a UAE bank, though the terms are stricter than for residents. Expect to put down 35 to 50 percent of the price, with banks lending the rest at rates that are usually a little higher than resident rates, over terms up to about 25 years. The bank will want your passport, proof of income, several months of bank statements and sometimes a salary certificate, and most lenders will not finance early-stage off-plan for non-residents. A practical structure many Indian buyers use is to send the down payment and fees from India under the LRS and take the UAE mortgage for the balance, which keeps the rupee outlay smaller in year one. Note that repaying a foreign loan also has its own remittance rules, so check with your bank. Our non-resident mortgage guide, linked below, covers eligibility, documents and the banks that lend.

Financing: can an Indian get a Dubai mortgage?

Yes. Indian buyers who do not live in the UAE can still get a non-resident mortgage from a UAE bank, though the terms are stricter than for residents. Expect to put down 35 to 50 percent of the price, with banks lending the rest at rates that are usually a little higher than resident rates, over terms up to about 25 years. The bank will want your passport, proof of income, several months of bank statements and sometimes a salary certificate, and most lenders will not finance early-stage off-plan for non-residents. A practical structure many Indian buyers use is to send the down payment and fees from India under the LRS and take the UAE mortgage for the balance, which keeps the rupee outlay smaller in year one. Note that repaying a foreign loan also has its own remittance rules, so check with your bank. Our non-resident mortgage guide, linked below, covers eligibility, documents and the banks that lend.

Property and a Golden Visa: the AED 2 million link

One reason Indian buyers stretch their budget toward the higher end is residency. A property worth AED 2 million or more qualifies you for a 10-year renewable Dubai Golden Visa, which lets you and your family live in the UAE, comes with no requirement to actually relocate, and survives long stays back in India. In 2026 that property can be mortgaged or off-plan, and the qualifying test is the property value rather than how much you have paid, so the visa is within reach of more buyers than before. From AED 1 million, buyers aged 55 and over can take a 5-year retirement visa instead. If residency is part of your plan, size your purchase with that AED 2 million line in mind; our dedicated Golden Visa guide, linked below, has the full eligibility detail and a separate checker.

Tax and reporting back in India

Buying abroad creates obligations back home, and getting this wrong is a common and avoidable mistake. As a resident Indian you must disclose foreign assets, including your Dubai property, in Schedule FA of your income tax return each year; this is a reporting requirement, not a tax on the asset itself, but non-disclosure carries serious penalties. Any rental income you earn in Dubai is taxable in India because residents are taxed on worldwide income, and you would claim relief for anything taxed in the UAE under the India-UAE tax treaty, though the UAE does not levy personal income tax on rent. When you eventually sell, capital gains may be taxable in India. The TCS collected on your LRS remittance is adjustable against this overall tax, as covered above. None of this should put you off, millions of Indians hold overseas property compliantly, but it does mean you should keep clean records of your remittances and the purchase, and run your situation past a chartered accountant. Tax rules change, so treat this as general guidance and confirm the current position before you file.

Mistakes Indian buyers make

The happy path is simple; these are the slip-ups that cost money or time.

- Ignoring the LRS limit and trying to send more than USD 250,000 per person in one financial year, which the bank will block.

- Treating the 20 percent TCS as a lost cost and over-budgeting, when it is adjustable against income tax.

- Forgetting to report the property in Schedule FA, which risks penalties far larger than any fee on this page.

- Sending money to an individual seller’s personal account in a resale without a trustee or proper escrow, instead of using the registration trustee office.

- Drafting a power of attorney that is too narrow or not properly attested for the UAE, so the representative cannot complete the transfer.

- Assuming a tourist or remote purchase gives residency; buying does not grant a visa unless the value reaches the AED 2 million Golden Visa threshold.

Sort these out before you transfer money, not after.

Free Property Valuation Dubai 2026 – Instant Property Price Estimate

About this guide

About this guide – Written by Md Arshad, SEO and Digital Marketing Manager – Real Estate at List My Properties. Last updated June 2026. How we verify: the remittance rules here are based on the Reserve Bank of India’s Liberalised Remittance Scheme and Indian income tax rules on foreign assets and TCS, and the Dubai purchase steps and fees on Dubai Land Department guidance current in 2026. LRS limits, TCS rates, tax reporting and property fees change, and individual cases vary, so confirm the current position with your bank, a chartered accountant and the DLD before you act. This is general information, not legal, tax or investment advice. Sources are listed in the external links section below.

Key takeaways

- Indians can buy freehold property in Dubai in 2026 with no UAE residency needed.

- Fund it under the RBI Liberalised Remittance Scheme, up to USD 250,000 per person each financial year; a couple can send USD 500,000.

- Remittances above INR 7 lakh attract 20 percent TCS, which is adjustable against your income tax, not a lost cost.

- You can buy entirely from India using a properly attested power of attorney.

- Budget about 6 to 8 percent over the price for fees, and report the property in Schedule FA at tax time.

- An AED 2 million property can also qualify you for a 10-year Golden Visa.

Tips and warnings

Pro tip 1: time your remittance across two financial years if your purchase exceeds your annual LRS room, or pool family members’ limits to move more in one year.

Pro tip 2: send the down payment and fees from India and take a UAE mortgage for the balance to keep your year-one rupee outlay smaller.

Warning 1: do not skip Schedule FA disclosure; the penalties dwarf any fee in this guide.

Warning 2: in a resale, pay through the registration trustee office, not into a seller’s personal account.

Insider tip: if residency matters, size your purchase toward AED 2 million so the same buy also earns a 10-year Golden Visa, rather than buying twice.

Trusted External Sources

- Reserve Bank of India, Liberalised Remittance Scheme: https://www.rbi.org.in/

- Income Tax Department of India: https://www.incometax.gov.in/

- Dubai Land Department: https://dubailand.gov.ae/en/

- ICP (Golden Residency): https://icp.gov.ae/en/services/golden-residency/

FAQs

Can Indians buy property in Dubai in 2026?

Yes. Indian citizens can buy freehold property in Dubai’s designated freehold areas in their own name, with no UAE residency or local sponsor required, and many buy entirely from India.

How much money can I send from India to buy property in Dubai?

Under the RBI Liberalised Remittance Scheme each resident can remit up to USD 250,000 per financial year, so a couple can send USD 500,000 and a family of four about USD 1 million toward a purchase.

Is there tax on sending money from India for a Dubai property?

Remittances above INR 7 lakh in a financial year currently attract 20 percent TCS. This is collected up front but is adjustable against your income tax, so it is a cash-flow item, not a permanent cost. Confirm the current rate with your accountant.

Do I have to travel to Dubai to buy property?

No. You can complete the entire purchase from India by giving a trusted person, a lawyer or your agent a properly attested power of attorney to sign and register on your behalf.

Do I need to report my Dubai property in India?

Yes. Resident Indians must disclose foreign assets, including Dubai property, in Schedule FA of the income tax return each year. Non-disclosure carries heavy penalties.

Can buying property in Dubai get me a visa?

A property worth AED 2 million or more qualifies you for a 10-year Golden Visa. From AED 1 million, buyers aged 55 and over can take a 5-year retirement visa. Smaller purchases do not grant residency.

Conclusion

Buying property in Dubai from India is well within reach in 2026 once you understand the two India-specific pieces: moving money under the LRS and, if you want, completing the deal remotely with a power of attorney. Set your budget with the planner above, keep clean records of every remittance, and line up your power of attorney early if you do not plan to travel.

Md Arshad

SEO & Digital Marketing Manager – Real Estate · Patna, India · MD Arshad is an SEO and digital marketing specialist focused on the real estate sector. He works as Digital Marketing Specialist at Dhruv Iconic Pvt. Ltd., a RERA-registered real estate company in Patna with 1.5+ years in the market, and has spent the last 0.5 years partnering with multiple real estate brands as a freelance SEO and content strategist. His work covers technical SEO, keyword research, competitor gap analysis, content strategy, and organic growth. He writes ListMyProperties guides to turn complex UAE real estate processes into clear, source-backed content, with every legal, tax, or fee claim referenced to official authorities such as DLD, RERA, DET, and the FTA. Connect on LinkedIn.